(Bloomberg) — Some of the best performing US debt in the first weeks of this year is the lowest rated, implying that corporate defaults are low on the list of investor fears now.

Debt rated in the CCC tier, the lowest ratings that commonly trade in the US, gained 1.15% this year through Thursday’s close on a total return basis. That’s better than just about every other kind of US debt, including other types of junk bonds. Treasuries are down about 0.2%, according to Bloomberg index data.

Most Read from Bloomberg

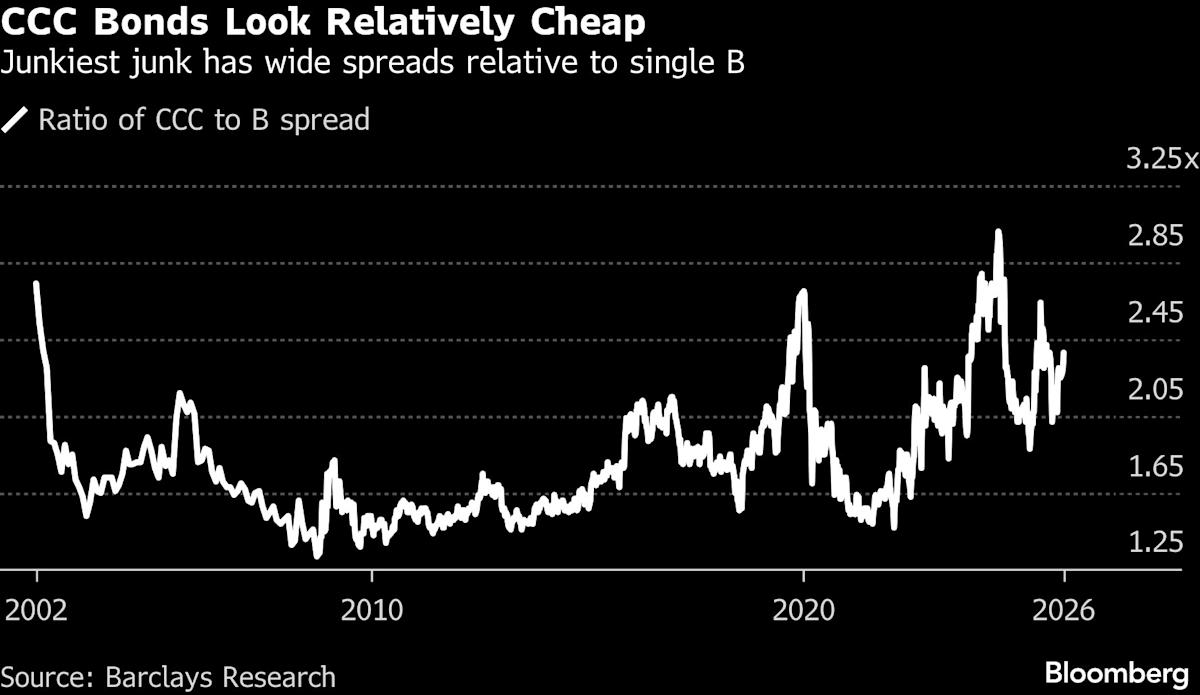

Some of the demand may be bargain hunting. According to Barclays, CCC debt is cheap by historical standards, based on the ratio of risk premiums for the bonds to the tier just above, in the B range. CCC outperformance this year comes after the bonds lagged other kinds of junk debt in 2025, gaining 8.3% last year while BB notes, for example, gained 8.9%.

“We believe the outperformance is because of market valuations,” said Sean Feeley, a high-yield portfolio manager at Barings. “The underlying economy is strong.”

The performance of the CCC part of the junk market is particularly important for junk bond investors, because it has an outsized impact on overall returns. According to Barclays, CCC notes account for about 12% of the high-yield index’s market value, but about a quarter of the spreads for the index.

“If you don’t invest in any CCCs you are going to get left behind,” said Michael Levitin, portfolio manager at MidOcean Partners.

The returns are coming at a time of growing disquiet in bond markets. Yields rose around much of the world this week, hurt by US President Donald Trump’s rhetoric about taking over Greenland, which threatens to undermine the world political order, and a tax cut pledge from Japanese Prime Minister Sanae Takaichi that tanked the country’s government bonds.

Even before the events of this week, US bonds had broadly been showing signs of pressure. The 10-year US Treasury yield has risen about 0.25 percentage point since late November, amid concerns that the Federal Reserve will be slower to cut rates with employment looking relatively strong.

Those rising yields are part of what has driven corporate bond demand in recent weeks. Money managers including pensions and insurance companies often focus on absolute yield levels when assessing investments, and are more inclined to buy when yields are higher.

They’ve been buying all kinds of corporate bonds. On Thursday, spreads on high-grade US corporate bonds reached 0.71 percentage point, or 71 basis points, the tightest since 1998. In the primary investment-grade market, companies have sold $170 billion of corporate bonds, up about 13% from the same time last year.

But money managers seem to have particular interest in junkier junk bonds in the US. In addition to gains in the secondary market, there have been six bond sales for CCC tier debt in January, totaling $3.5 billion, about 15% of total high-yield supply. In the first month of last year, there were two sales, totaling $630 million, amounting to around 3% of junk issuance.

“People want the yield, they need the paper and they have cash,” said MidOcean’s Levitin.

The CCC market is split between better performing securities that are trading at relatively expensive valuations, and bonds at greater risk of default trading at distressed levels, said Corry Short, a strategist at Barclays.

“Because of the degree of dispersion within the CCC segment right now, you have to look through a more narrow lens when trying to identify relative value in CCCs, and it makes credit selection paramount,” Short said.

Investors are broadly making a distinction between companies growing robustly, and those with more limited potential to perform well. Corporations with higher growth might also have strong equity profiles, said Scott Hague, head of global leveraged finance and private credit at TD Securities.

“In this kind of environment, it’s not unusual to see spreads for stronger credits compress to levels normally reserved for comparable single B rated names,” Hague said.

Click here for a podcast on “credit zombies” with Seix Investment Advisors

Week In Review

Some companies put debt offerings on hold after tensions between the US and Europe over Greenland and a selloff in Japanese bonds unnerved global markets. It was a dramatic shift from the frenetic pace of debt offerings seen earlier in January, typically one of the busiest months for primary markets.

After largely grinding to a halt, debt markets sprang back to life as President Donald Trump’s sudden reversal on Greenland helped revive risk appetite. The so-called TACO trade lifted sentiment, with more than $23 billion of bonds pricing across the US and Europe on Wednesday.

US regional banks also seized on calmer waters, racing to the investment-grade debt market for funding and underscoring a rebound in risk appetite.

Distressed-debt giants Oaktree Capital Management and Anchorage Capital have amassed positions in the bankruptcy financing for First Brands Group, stepping in as negotiations over a fresh capital injection for the auto parts supplier come down to the wire.

Some China Vanke dollar bondholders are urging the distressed builder to consider options such as debt-to-equity swaps, as they seek to avoid getting sidelined in what would be one of the country’s largest-ever restructurings.

Buyout firm Hg is in discussions with private credit lenders for a roughly $3 billion loan to help finance its acquisition of OneStream Inc.

RSA Security, co-owned by Clearlake Capital Group and Symphony Technology Group, is embarking on a distressed exchange with total debt discounts of about $400 million.

Tailored Brands, the parent company of Men’s Wearhouse, boosted its loan and bond offerings by a combined $200 million to fund an even larger dividend payout to its owners.

Kyma Capital, a hedge fund run by Akshay Shah, delivered 48% net returns to investors last year, betting on distressed companies needing to address their debt piles.

Banks were so eager to get a piece of the jumbo debt package backing Netflix Inc.’s bid for Warner Bros. Discovery Inc. that some have been left with a smaller slice of the deal than they wanted.

Paper and packaging producer Pro-Gest SpA reached a deal with Carlyle Group Inc. and a majority of its bondholders to address its defaulted debt pile after more than a year of negotiations.

On the Move

Millennium Management is creating a new credit trading unit, carving it out from its fixed income business. The unit will be led by Dan Friedman, reporting to Millennium’s co-chief investment officer Justin Gmelich.

Goldman Sachs Group Inc. is making leadership changes across its global credit business. Veteran partner Christina Minnis will become global head of the bank’s alternatives origination group, while fellow partner Miriam Wheeler is taking over as global head of leveraged finance.

JPMorgan Chase & Co. named Simon Dale as its global head of the credit portfolio group lending, a team that manages regulatory capital using tools such as synthetic risk transfers. Dale replaces William Ledger, who has spent more than three decades at the bank.

Sumitomo Mitsui Banking Corp. has seen another senior banker departure in Asia, amid ongoing internal changes. Kyoko Murai, head of origination for South and Southeast Asia in the bank’s loan capital markets division, left last week.

–With assistance from Gowri Gurumurthy and James Crombie.

Leave a Reply