January 16, 2026

5 min read

Key takeaways:

- ACA subsidies were launched in response to the COVID-19 pandemic.

- Uninsured and underinsured patients skip or delay care until emergencies happen.

- Hospitals will face a surge in uncompensated care.

For the past several years, millions of Americans have relied on a policy many are not familiar with: enhanced Affordable Care Act subsidies that made health insurance affordable.

Those subsidies are now expiring, and they only made the national spotlight during the latest government shutdown. The consequences will be swift, severe and widely felt not just by patients, but also by an already strained health care system.

Data derived from Hanson C, et al. Health Aff (Millwood). 2023;doi:10.1377/hlthaff.2023.00325 and Levitt L. JAMA Health Forum. 2026;doi:10.1001/jamahealthforum.2025.6929.

Millions will lose coverage. Hospitals already on the brink will face financial and operational strain, recreating the all-too-familiar scene of families sitting for hours in emergency waiting rooms, watching conditions worsen while beds remain unavailable.

What this means for patients

At its core, the expiration of enhanced ACA subsidies is about affordability.

Owais Durrani

During the pandemic, Congress temporarily expanded subsidies so more Americans, including many middle-income families, could purchase health insurance without paying an unsustainable share of their income.

The policy worked. Enrollment in ACA Marketplace plans reached record highs, and millions of people who previously fell through the cracks gained coverage. Now, that progress is at risk of unraveling.

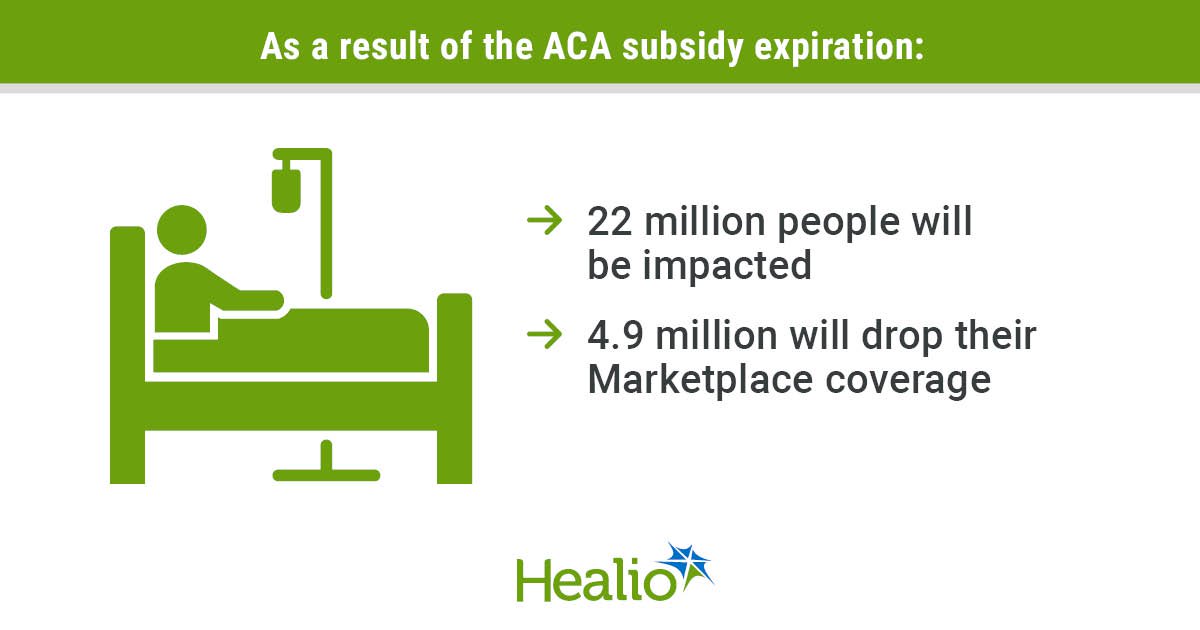

Twenty-two million Americans are projected to be impacted by a loss of enhanced subsidies. Premiums for many Marketplace enrollees are expected to rise sharply and even double in some cases.

It also is estimated that 4.9 million people will drop their Marketplace insurance coverage. Instead, they will enroll in unsubsidized nongroup coverage or coverage based on their employment, or they will become uninsured. For families already stretched thin by housing costs, food prices and student loans, the coming increase is a breaking point.

The result is predictable and well documented. Uninsured or underinsured patients delay care, skip medications and postpone management of chronic conditions such as diabetes, asthma or heart disease until those conditions become emergencies. This is a prescription for disaster, not only worsening outcomes for patients but also increasing total costs.

Some argue that the enhanced ACA subsidies were originally a response to the financial strain of the pandemic, which has now ended. However, the underlying affordability challenges in health care that were exacerbated by the pandemic have not disappeared.

Many households continue to face persistent economic aftershocks such as inflation, wage stagnation and rising insurance premiums. Continuation of the subsidies therefore remains critical not as a temporary crisis response, but as an ongoing investment in maintaining access to care and preventing cost-driven coverage losses.

Health insurance doesn’t just pay bills. It determines when, where and whether people seek care at all. Taking it away, or making it unaffordable, is not a neutral policy choice. It directly shapes population health, with stark consequences that can mean life or death.

Strain in the ED

When people lose coverage, they don’t just disappear from the health care system. They re-enter it through the most expensive, least efficient door: the ED.

EDs are already under extraordinary pressure. Many are dealing with staffing shortages, record boarding times and rising patient acuity. Adding more uninsured patients, particularly those who delayed care, will worsen crowding, lengthen wait times and stretch clinicians thinner.

This isn’t just inconvenient. Overcrowded EDs are associated with higher rates of medical errors, delays in time-sensitive interventions and worse overall outcomes. Boarding patients for hours or days in hallways is not just demoralizing for staff. It’s dangerous for patients.

Hospitals, especially safety-net and rural facilities, will also face a $7.7 billion surge in uncompensated care in 2026. Analysts also estimate that the expiration of ACA subsidies could cost health care providers $32.1 billion in lost revenue.

For institutions already operating on razor-thin margins, that loss can mean service cuts or facility closures, creating a negative spiral. This is how policy decisions in Washington quietly reshape life and death far from the Capitol.

Finally, having more uninsured patients also results in disruptions in continuity of care. Patients switching insurance plans or cancelling coverage often lose access to their physicians. The result is predictable. Medications are interrupted. Follow-up appointments are missed. Chronic disease management becomes episodic rather than proactive.

The irony is painful. The system ends up spending more money treating advanced disease that could have been prevented or managed earlier if coverage had been affordable in the first place.

How we got here

The current crisis was not inevitable, but it was predictable.

Robert Glatter

The Affordable Care Act, passed in 2010, created health insurance marketplaces with subsidies to make coverage affordable. During the COVID-19 pandemic, Congress expanded those subsidies through the American Rescue Plan, eliminating income cliffs and increasing financial assistance. The Inflation Reduction Act later extended the subsidies through the end of 2025.

Those enhancements were enormously successful. Enrollment surged, and gaps in coverage narrowed. Yet despite their effectiveness, the subsidies were never made permanent. They were treated as a temporary budget item rather than a foundational part of the health care system.

As the expiration date approached, political gridlock won. Efforts to pass an extension failed, caught in broader budget battles and ideological disputes over the role of government in health care.

Choice, not an accident

What makes this moment especially troubling is that the consequences are well understood. We know what happens when people lose insurance. We know what happens to EDs when access to primary care erodes. We know what happens to hospitals when uncompensated care rises.

Allowing the subsidies to expire is not an act of fiscal prudence. It is a cost shift from federal budgets to families, hospitals and local communities. The money doesn’t disappear. It reappears, albeit in a greater sum, as medical debt, delayed diagnoses, avoidable hospitalizations and systemic strain.

At this point, Congress went home for the holidays and decided not to act, although it is back in session now. Expiration of the subsidies will lead to increased uncertainty and lack of enrollment, resulting in harm that will take years to undo.

Yash B. Shah

The expiration of ACA subsidies is not just a rollback of a pandemic-era policy. It is a stress test of whether the U.S. health care system values stability, prevention and access or continues to tolerate a cycle of crisis and reaction.

If we allow millions to lose coverage, the damage won’t be limited to insurance markets. Massive numbers of people will face medical emergencies, overwhelming hospitals and impacting communities already stretched to their limits.

Policymakers still have options: extending the subsidies, redesigning them or preventing the abrupt loss of coverage. What they no longer have is the excuse of uncertainty.

This is the cliff. We’re standing at the edge. And the fall will be felt by all of us.

For more information:

Owais Durrani, DO, an emergency medicine physician with the Memorial Hermann Health System, can be reached at allergy@healio.com and on LinkedIn, Instagram, YouTube and X. Robert Glatter, MD, assistant professor at the Zucker School of Medicine at Hofstra/Northwell and an emergency medicine physician at Lenox Hill Hospital, can be reached at rglatter@northwell.edu and on Instagram, LinkedIn and X. Yash B. Shah, MD, a resident in the department of surgery at Penn Medicine, can be reached at yashah01@gmail.com and on X.

Sources/Disclosures

Source:

Expert Submission

References:

Disclosures:

Durrani and Shah report no relevant financial disclosures. Glatter reports holding membership on the CaringKind board of directors.

Ask a clinical question and tap into Healio AI’s knowledge base.

- PubMed, enrolling/recruiting trials, guidelines

- Clinical Guidance, Healio CME, FDA news

- Healio’s exclusive daily news coverage of clinical data

<

Leave a Reply